Everybody Gets A Card!

Advances in Consumer Fintech

The consumer financial technology world is transforming at an incredible pace. It’s never been easier to set up an online shop, transfer funds, and invest in assets that didn’t exist five years ago. Restaurants are rapidly adapting to contactless payments while loans are processed and delivered immediately. While all this is significant, we’re still in the first stage of this evolution and big changes are coming to how we bank, create products, and make decisions.

People are accustomed to standard financial apps where you check balances, transfer money, pay off loans or buy stocks. The new generation of fintech apps are starting to feel like social media platforms: intuitive, dynamic, and fun. In due time, these apps will increasingly automate investments, connect users to unique experiences, and ultimately provide avenues to increase income.

Infrastructure Is The Catalyst

Before cloud services like AWS & Microsoft Azure were established, launching a simple e-commerce or media website required a ton of cash as well as time to set up and maintain in-house servers. Today, it’s nearly free and takes no time to get started. Likewise, the infrastructure pieces required to start a financial business are rapidly becoming “productized”.

What does that mean? What used to make starting a financial services company so difficult, like adding bank accounts, transferring money, issuing cards, buying stocks, etc. is now a service you can sign up and integrate into your platform with few lines of code. Enormous engineering and operational initiatives that would take months to complete now take a few days or less (sometimes minutes!).

The consumer opportunity lies in building on top of these core components in a way that prioritizes usability for folks of all socioeconomic levels.

Starting From The Bottom

Six percent of adults do not have a checking, savings, or money market account (often referred to as the "unbanked"). Two-fifths of unbanked adults used some form of alternative financial service during 2018—such as a money order, check cashing service, pawn shop loan, auto title loan, payday loan, paycheck advance, or tax refund advance.¹

These are all nightmare ways to hold or send money. Unfortunately, unbanked and underbanked folks feel as though the big financial institutions are scheming against them. In many cases, it’s true that “it’s expensive to be poor.” Banks punish account holders with fees for late payments, transfers, low balance, overdraft, inactivity, and even closing an account!

Because challenger bank startups, often called neobanks, don’t have to worry about maintaining real estate (no physical locations), they can bring these cost savings to people by waiving annoying fees, and instead get ahead of the curve with practical features like early advances, daily paychecks, quick loans, and much more.

In the 2020 covidcopalypse, offline to online transformation is a forced reality. And new behaviors that are cheaper and easier than the previous method tend to become habits. We’ll continue to see more digitization as apps better optimize for people of all income levels.

Financial Products For All

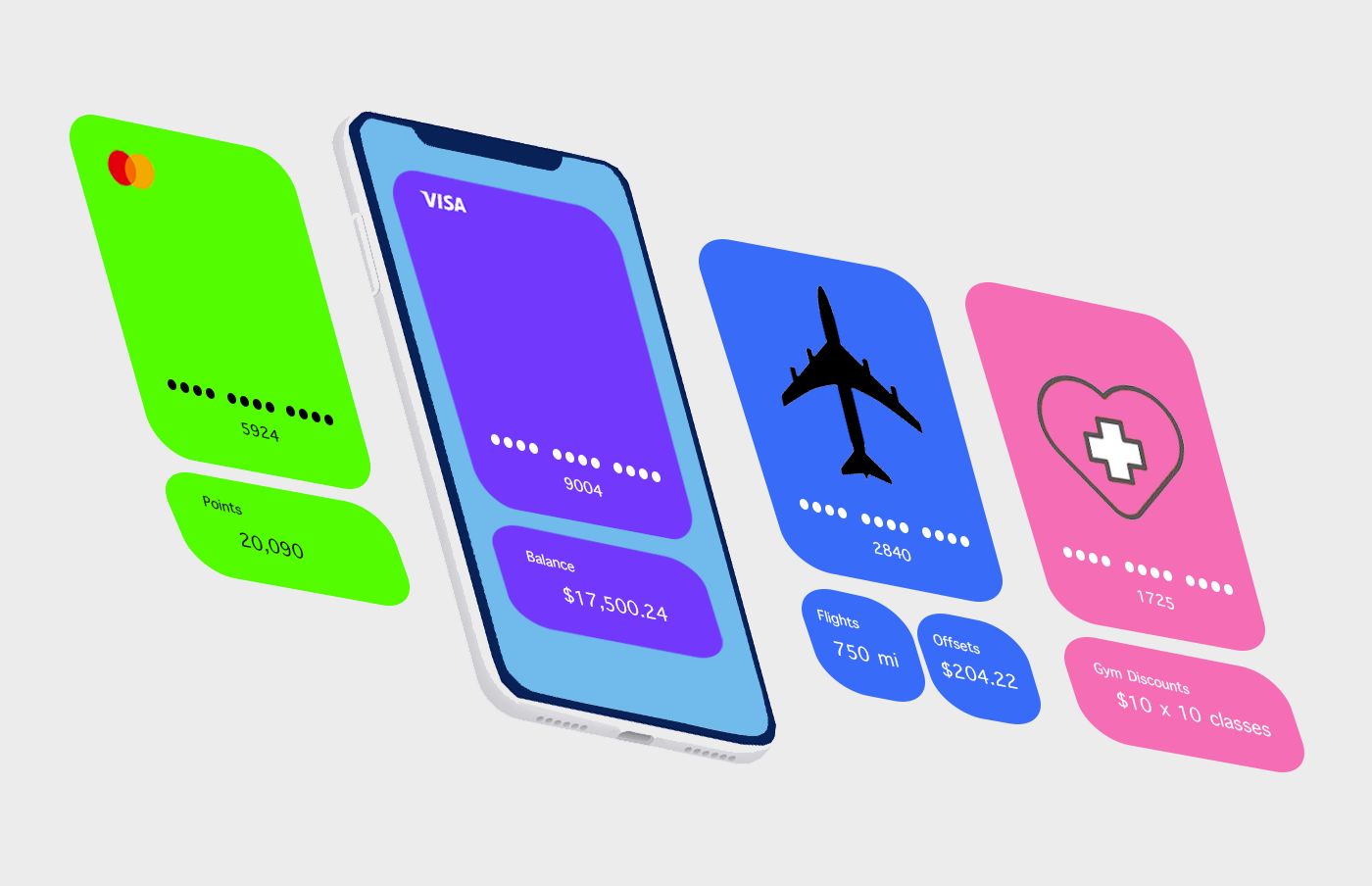

Through card issuing offered by payment services like Marqueta or Stripe, companies can deploy virtual and physical cards for their users. The ease of doing so enables any business, not just those in finance, to build domain-centric financial products for their customers. This is a monumental win-win for both firms and consumers for a variety of reasons.

For example, an airline can offer a card that buys carbon offsets with every purchase. A health insurance company can launch a card that rewards customers with discounts for healthy food purchases and fitness classes. In return, companies will be able to incentivize new customer sign-ups and have access to spending data. With this insight, they can launch more financial products, like lending or insurance coverage. These offerings will empower businesses in all sectors to understand and engage their customer base at a granular level, while people benefit through personalized benefits and lower costs.

“Never Discuss Money In Public!”

Millenials and Gen Z are the main targets for new products in fintech because the rising generations are far more comfortable talking about things like salary, what they are spending on, and how much debt they have to pay off.

Why? Because today, everything is really expensive! The majority of young people aspire to live in and around cities. However, It's really challenging to buy a nice house through conventional career growth like past generations could. Young people today don’t just think about their day job, but work to create multiple income streams through investing and monetizable side projects.

Nearly everything we do is an act of signaling, whether it’s the brands we wear, places we travel, or career paths we pursue. The popular social networking platforms like facebook, instagram and linkedin have trained us to signal our actions to one another online. This habit has creeped into financial platforms.

Venmo, a popular money transfer app, has a public feed that exposes a social graph of people’s transactions. There're many popular ways to send payments, but Venmo captured the rising generations by captioning payment transfers with expressions like emojis. Went out for dinner/drinks? One person pays and the others Venmo them back. Fun and simple.

Some of the biggest opportunities in consumer fintech will be discovered by setting aside the older generations’ social stigma around expenses and see what sticks. This could be in-network leaderboards to compete on who paid the most for food delivery, who racks up the most Uber rides, or who’s setting aside the most cash for the Cabo trip; tons of combinations to try.

Adding Wealth

The ultimate goal of consumer financial apps is to complete the cycle of income to expenses, savings, and investing. Managing finances is helpful, but assisting users make more money is key. In our current economic reset, some sectors are able to go remote and it’s business as usual, but many have to go back to the drawing board and rethink how to operate. it's never been more clear that people shouldn’t be dependent on full time jobs for their only income - it can go away just as easily as it came. Neobanks and other financial apps are stepping in to help build the tools to find new jobs or start a business. Providing the avenues to reach or surpass their financial goals will create lifelong happy consumers.

- Like thinking about this stuff? Want to discuss it further? Let me know as I’m working on some fun projects in the consumer fintech space.

- Thanks Sheel Mohnot and Morgan O’Connor for reading drafts of this essay.

Sources: